Retire Before 65: Why Tax Diversification Matters More Than You Think

Retire Before 65: Why Tax Diversification Matters More Than You Think

When people talk about retiring before 65, the conversation usually centers on how much money you need. That’s understandable, but incomplete.

The more important question is often where your money lives and how it’s taxed when you use it.

Early retirement doesn’t fail because people didn’t save enough. It fails because money is locked in the wrong places at the wrong times.

Early Retirement Is a Tax Planning Problem First

Retiring before 65 creates a different financial reality than traditional retirement:

- You may stop working years before Social Security begins

- You’ll likely need income before age-based retirement rules kick in

- You’ll have more years where taxes can quietly erode progress

This makes tax flexibility, not just investment growth, one of the biggest drivers of success.

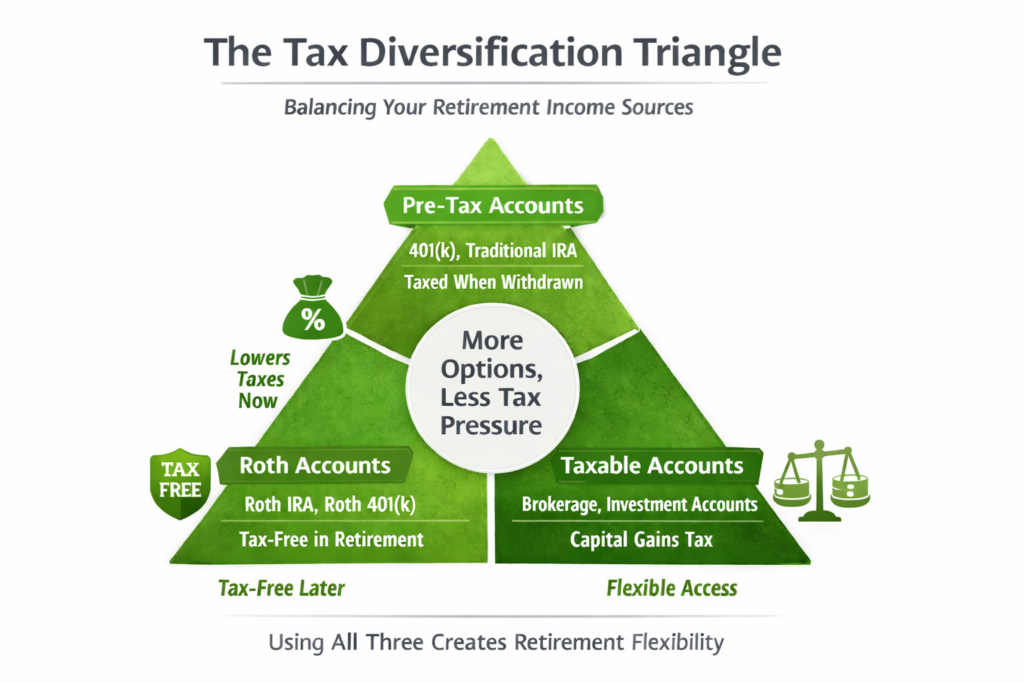

The Three Types of Accounts That Create Flexibility

A strong early-retirement plan usually includes multiple types of accounts, each with different tax rules. This isn’t complexity for complexity’s sake, it’s about control.

Qualified (Pre-Tax) Retirement Accounts

Examples include traditional 401(k)s and traditional IRAs.

These accounts:

- Reduce taxable income while you’re working

- Grow tax-deferred

- Are fully taxable when withdrawn

They’re excellent accumulation tools. The downside shows up later if all retirement income must come from taxable withdrawals, especially in years when you’re trying to keep income low.

Roth and After-Tax Retirement Accounts

This bucket includes Roth IRAs and Roth 401(k)s.

These accounts:

- Are funded with after-tax dollars

- Grow tax-free

- Can provide tax-free income in retirement

Roth accounts give you timing control. You’re not just saving money, you’re choosing when taxes are paid. That choice becomes powerful in early retirement years with lower income.

Non-Qualified / Brokerage Accounts

Brokerage accounts don’t get the spotlight they deserve in retirement conversations.

These accounts:

- Have no age restrictions on access

- Are typically taxed at capital gains rates

- Can fund the gap between work and traditional retirement age

For many people aiming to retire before 65, this bucket is the bridge that makes early retirement realistic without penalties or forced withdrawals.

Why Multiple Account Types Change Everything

When all your savings sit in one tax category, your retirement income becomes rigid. You take what you must, when you must, and pay whatever taxes come with it.

When savings are spread across account types, you can:

- Choose which dollars to use each year

- Keep taxable income within desired brackets

- Manage lifetime taxes, not just annual taxes

- Adjust when tax laws or life circumstances change

This flexibility often determines whether early retirement feels freeing—or financially stressful.

The Overlooked Advantage of Early Retirement Years

One of the biggest missed opportunities in early retirement is low-income tax planning.

Before required minimum distributions begin and before Social Security starts, many retirees have a window where income can be strategically managed. Having access to different account types allows those years to be used intentionally rather than wasted.

This Is About Control, Not Complexity

Tax diversification doesn’t mean owning every account type or chasing loopholes. It means building a plan that:

- Matches savings to life stages

- Anticipates income timing

- Reduces forced decisions later

The earlier this is addressed, the more gradual—and less painful—the adjustments can be.

How the Being Financial Team Approaches Early Retirement Planning

At Being Financial, early retirement planning isn’t built around a single number or age. It’s built around timing, values, and flexibility.

Our approach integrates:

- Investment strategy

- Tax planning over decades, not just annually

- Real-life transitions like career changes, caregiving, and burnout

The goal isn’t just to retire early. It’s to retire with options and confidence.

Final Thought

Retiring before 65 isn’t reserved for extreme savers or perfect planners. It’s most often achieved by people who:

- Start early enough

- Avoid locking all savings into one tax bucket

- Understand that taxes don’t disappear in retirement—they change

A well-structured plan doesn’t just help you retire sooner. It helps you stay retired on your own terms.

For readers who would like to explore this topic further, we’ve created a short resource: Practical Guide to Avoiding the Early Retirement Tax Trap. This guide provides additional context around tax diversification and highlights several factors individuals often review when evaluating early retirement decisions. Download the guide if you would like a deeper overview of these concepts.

Looking for more clarity on your retirement tax strategy? Contact us to schedule a 1-0n-1.